For Everyday Payment Problems

and easy configuration to create a number of different payment solutions.

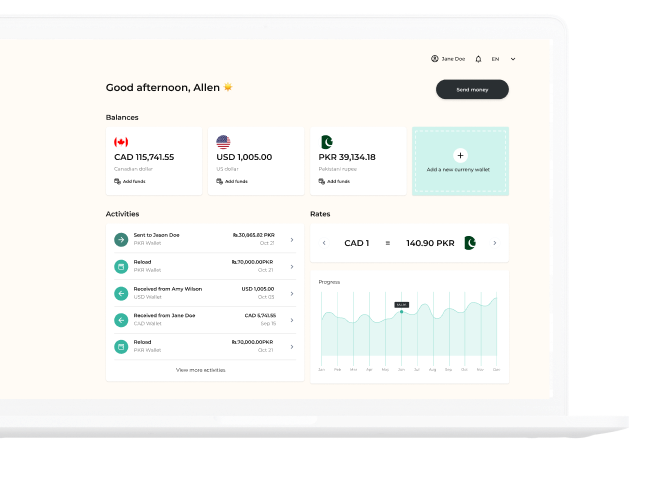

solutions with send and request money

capabilities featuring data rich and traceable

ecommerce and mobile payments.

For Everyday Payment Problems

and easy configuration to create a number of different payment solutions.

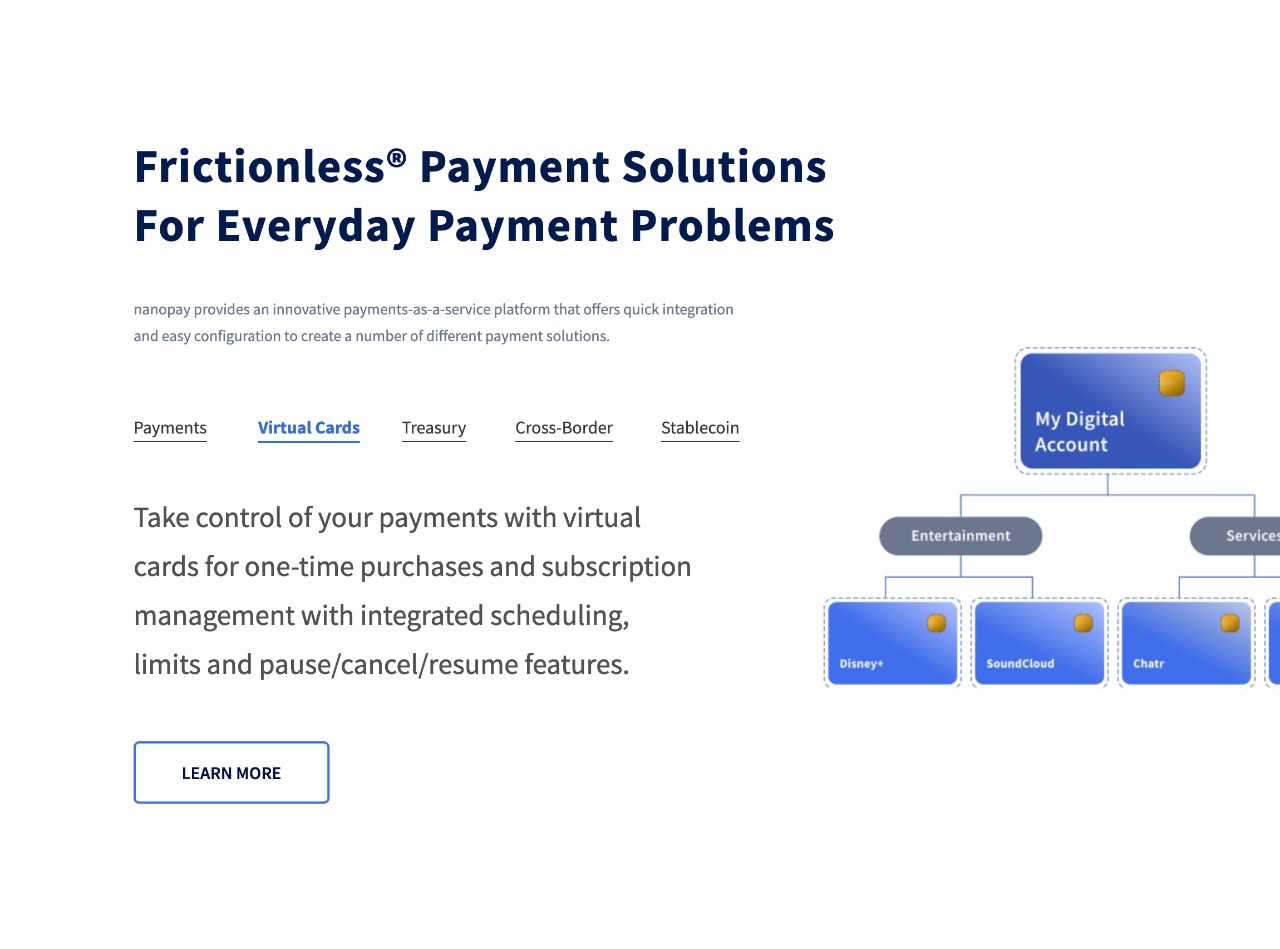

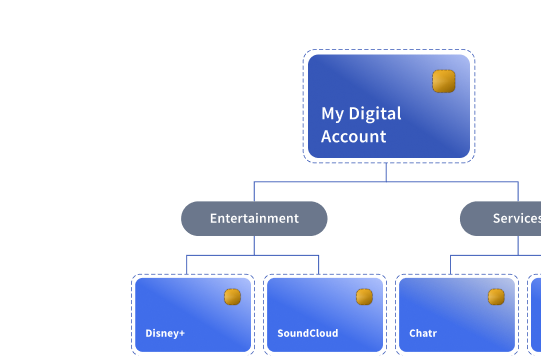

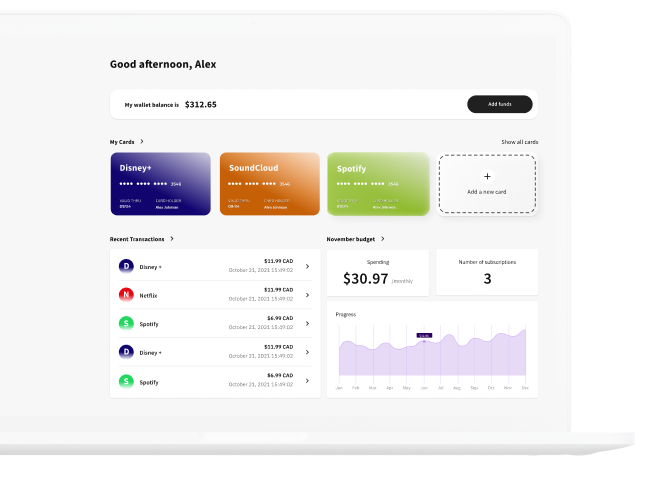

cards for one-time purchases and subscription

management with integrated scheduling,

limits and pause/cancel/resume features.

For Everyday Payment Problems

and easy configuration to create a number of different payment solutions.

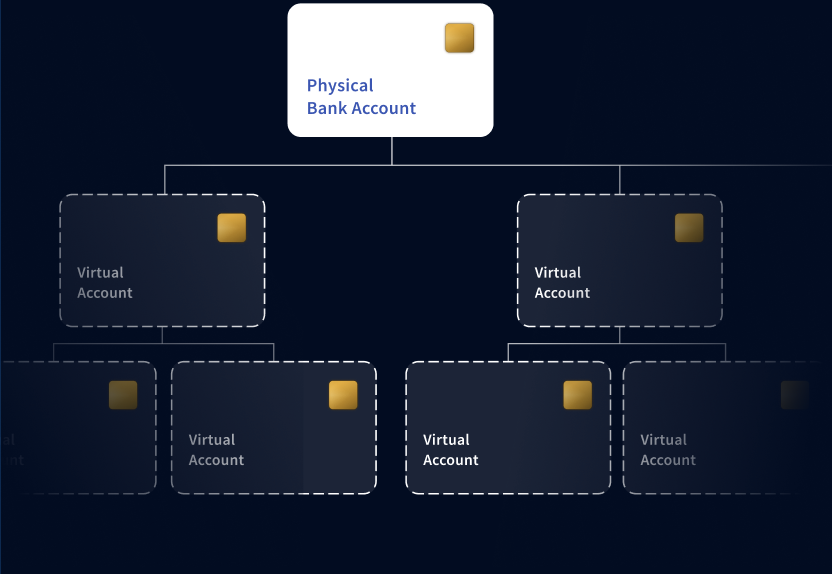

solutions built on a virtual account

ecosystem to net, pool funds, and better

manage payables and receivables.

For Everyday Payment Problems

and easy configuration to create a number of different payment solutions.

including remittance, payroll and bill

payments with competitive FX rates and

configurable fee options.

For Everyday Payment Problems

and easy configuration to create a number of different payment solutions.

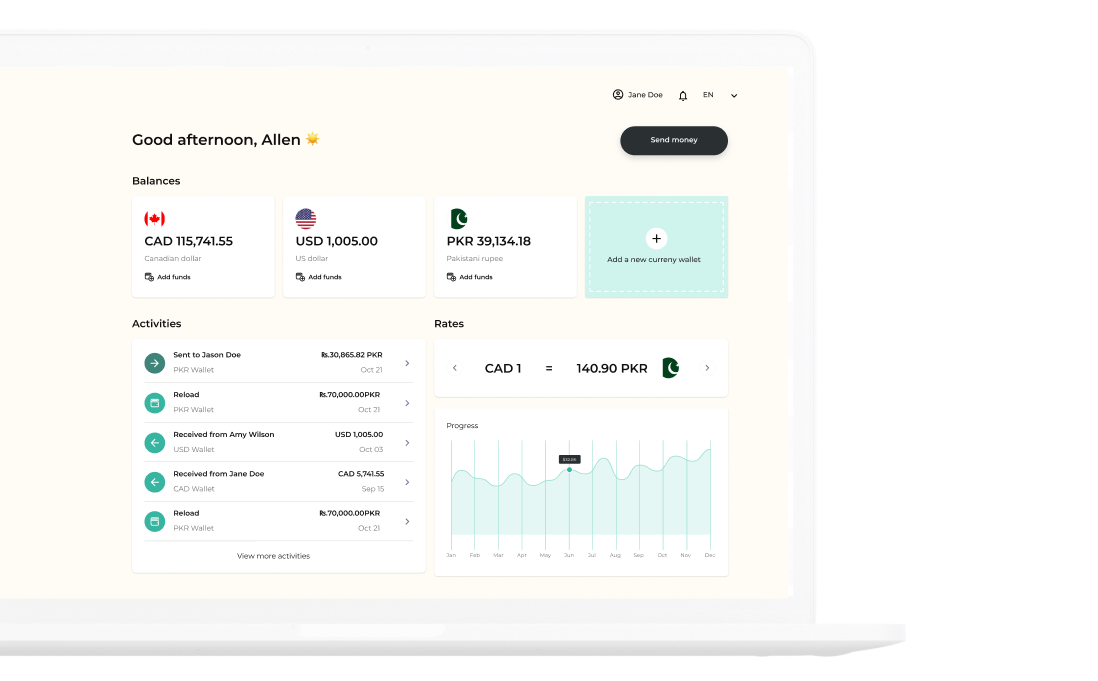

with value centrally stored in digital wallets

that power applications to send, request

and receive digital payments instantly.

For Everyday Payment Problems

platform that offers quick integration and easy configuration

to create a number of different payment solutions.

solutions with send and request money

capabilities featuring data rich and traceable

ecommerce and mobile payments.

For Everyday Payment Problems

platform that offers quick integration and easy configuration

to create a number of different payment solutions.

for one-time purchases and subscription

management with integrated scheduling, limits

and pause/cancel/resume features.

For Everyday Payment Problems

platform that offers quick integration and easy configuration

to create a number of different payment solutions.

solutions built on a virtual account

ecosystem to net, pool funds, and better

manage payables and receivables.

For Everyday Payment Problems

platform that offers quick integration and easy configuration

to create a number of different payment solutions.

including remittance, payroll and bill

payments with competitive FX rates and

configurable fee options.

For Everyday Payment Problems

platform that offers quick integration and easy configuration

to create a number of different payment solutions.

with value centrally stored in digital wallets

that power applications to send, request and

receive digital payments instantly.

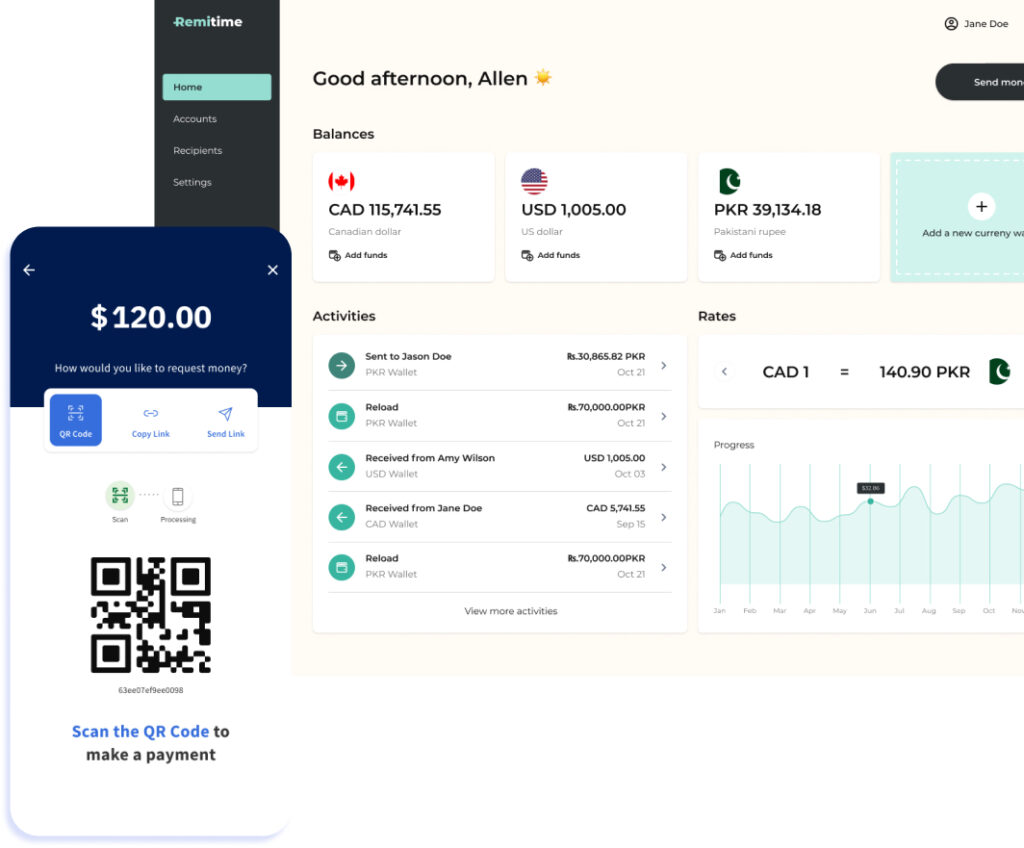

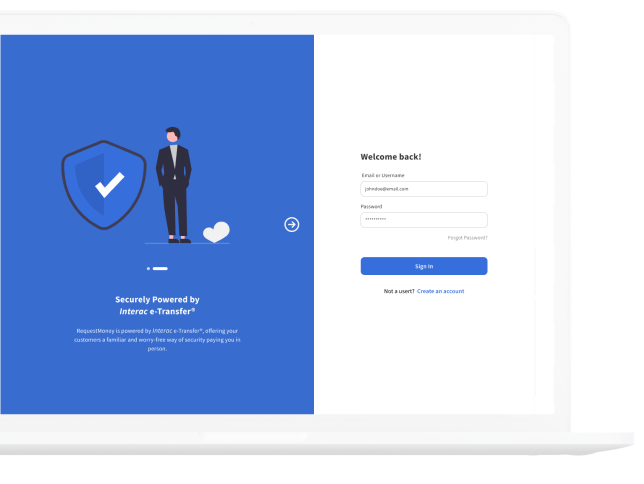

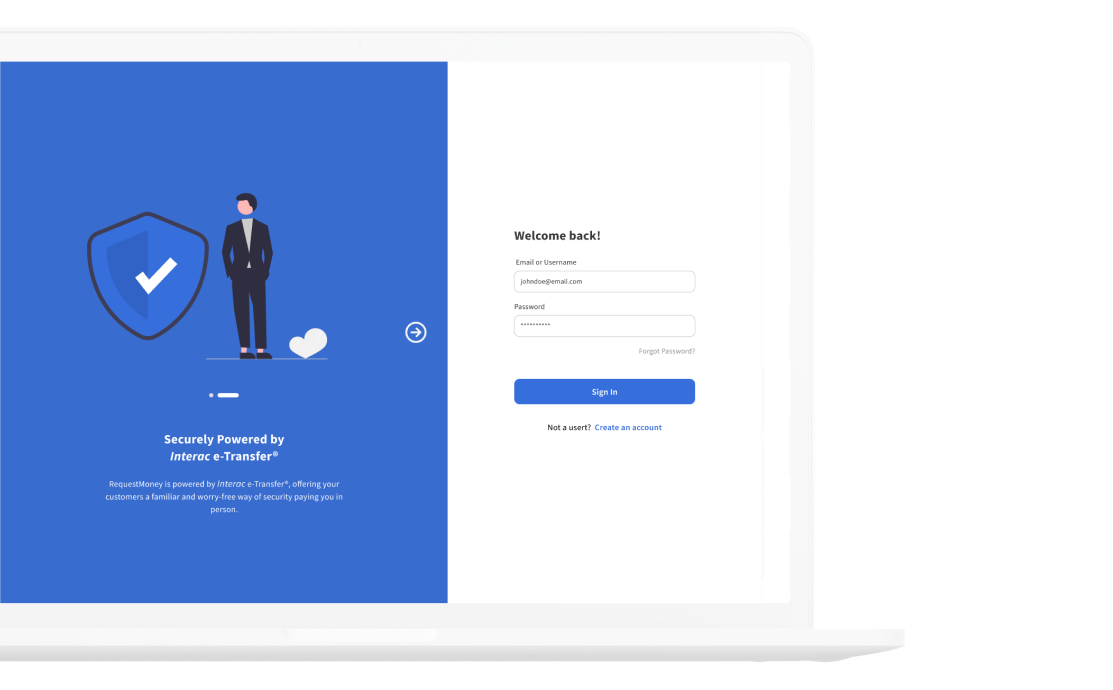

Way to Get Paid

directly from their bank. Powered by Interac e-Transfer®,

Requestmoney provides your customers with a familiar

and worry-free way to pay you in-person or email.

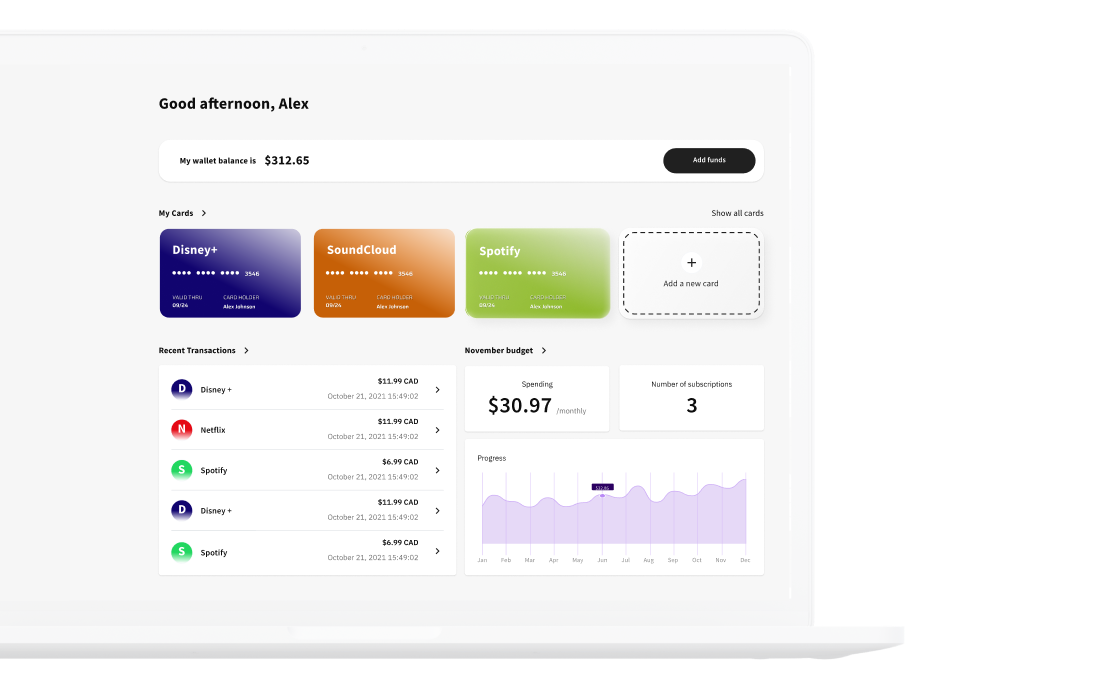

Rule Them All

subscriptions directly from the Cardmeleon app. Set up

custom schedules, and spend limits; pause, resume, or

cancel cards any time you want.

Border Free

customers to send cross-border payments whether they

are individuals or businesses.

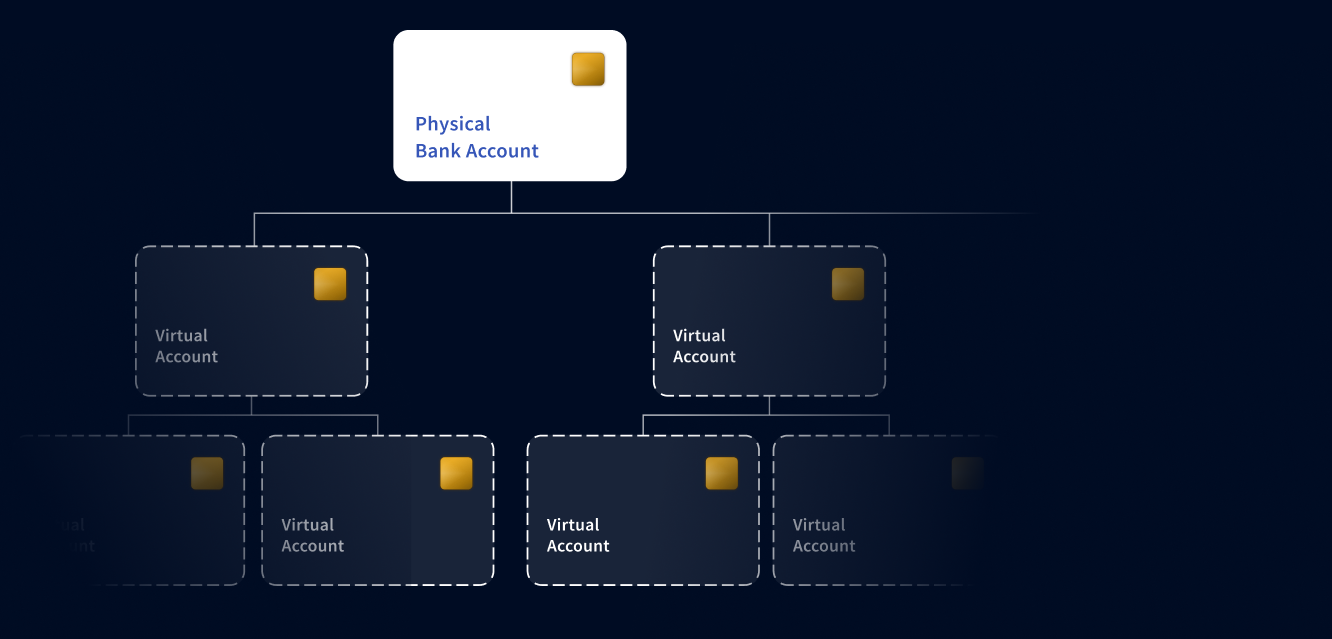

Made Easy

Management solution that provides complete visibility,

simplifies payment reconciliation and improves financial

reporting - without the fees and complexities of

maintaining many physical bank accounts.

pay you directly from their bank. Powered by

Interac e-Transfer®, Requestmoney provides

your customers with a familiar and worry-free

way to pay you in-person or online.

Way to Get Paid

or recurring subscriptions directly from the

Cardmeleon app. Set up custom schedules,

and spend limits; pause, resume, or cancel

cards any time you want.

Rule Them All

to enable your customers to send cross-border

payments whether they are individuals or

businesses.

Border Free

Account Management solution that provides

complete visibility, simplifies payment

reconciliation and improves financial reporting -

without the fees and complexities of maintaining

many physical bank accounts.

Made Easy